Investors Hit the Panic Button Ahead of Nonfarm Payrolls

- Dollar turns its sights to another decisive US employment report

- Yen slips as Bank of Japan refuses to tighten, gold tries to recover

- Stock markets fall sharply as financial contagion fears infect banks

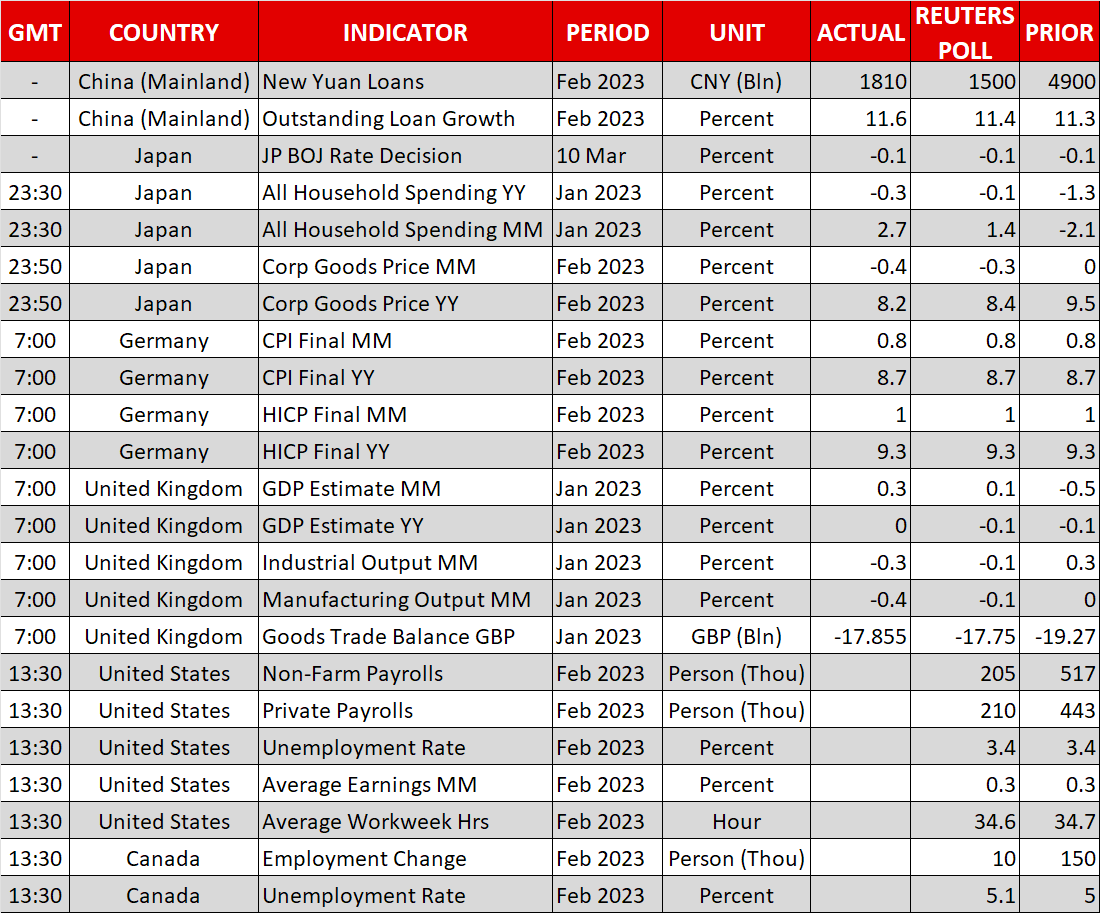

Nonfarm payrolls, high stakes edition

It has been a stormy week for financial markets, characterized by turmoil in interest rates and stocks. Some hawkish remarks by the Fed chief served as the trigger for this wave of volatility, after he warned that the ultimate level of interest rates might be higher than previously assumed to defeat inflation.

Money markets are currently pricing in almost 50-50 odds on whether the Fed will raise rates by a quarter or a half percentage point in two weeks. This means the stakes surrounding today’s US employment report are even higher than usual, as any surprises could tip the scales in one direction and drive markets accordingly.

The tea leaves point to another solid month for the US labor market. Business surveys hinted at a reacceleration in hiring, applications for unemployment benefits remained historically low, and the private ADP report exceeded expectations. All of this lends credibility to the official forecast, which suggests nonfarm payrolls will print 200k in February after a stunning 517k last month.

Nonetheless, there is a risk of disappointment. When a nonfarm payrolls print is as strong as it was last month, it is often followed by a softer number — a correction back to the prevailing trend essentially. That might be particularly true this time, considering that warm weather and seasonal adjustments played a big role in boosting the previous number.

Therefore, there might be some ‘payback’ in this report. A disappointment could inflict some damage on the dollar, but is unlikely to be a game changer for the broader trend as most metrics suggest the jobs market is still in good shape overall.

Yen retreats as investors say sayonara to Kuroda

The Bank of Japan did not adjust its policy settings at Governor Kuroda’s final meeting, disappointing traders who were betting on another increase in the yield ceiling and dealing a blow to the Japanese yen. At the heart of this decision was the belief that inflationary pressures are not durable, as the energy subsidies that were rolled out recently have already pushed Tokyo’s inflation rate sharply lower.

But while the yen is down, it is not out. Preliminary results of the spring wage negotiations between labor unions and big businesses point to wage increases above 5%, an outcome that probably exceeds the Bank of Japan’s wildest dreams and thereby sets the stage for further tightening as early as next month when Kazuo Ueda takes over as governor.

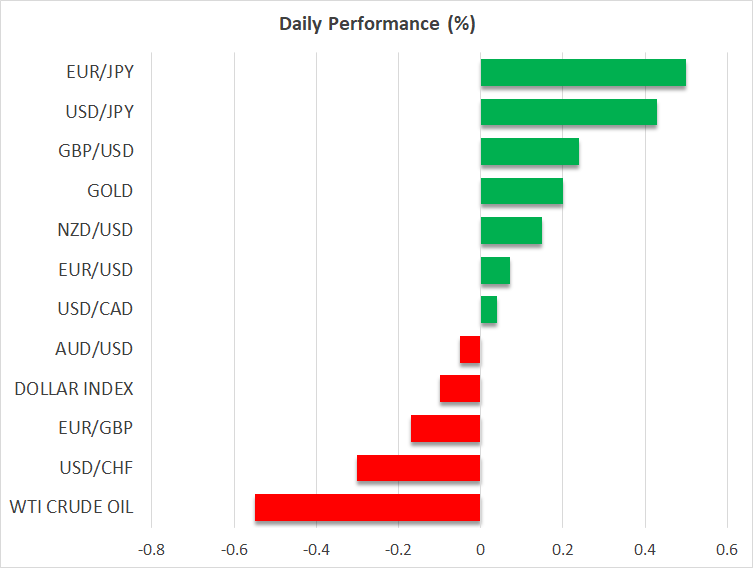

In the commodity space, gold prices staged a comeback yesterday. Bullion gained around 1% as the instability in equity markets sparked a flight to safety, pushing investors into the security of haven assets such as bonds and gold.

Bank stocks lead Wall Street lower

Some glimpses of panic selling appeared in stock markets yesterday. The S&P 500 lost 1.85%, with shares of banks getting decimated as worries around the health of the financial system emerged.

The epicenter of this selloff was SVB Financial Group, whose shares cratered by 60% and are down another 28% in premarket trading on Friday amid concerns about the solvency of its banking arm that focuses on venture capital clients. The mere risk of failure at a major financial institution was enough to reawaken old nightmares of contagion on Wall Street, leading to a ‘sell first, ask questions later’ trading dynamic.

So far, the selloff has been concentrated in financial stocks as investors try to work out the probability of default and whether the bank’s footprint is large enough to cause systemic problems.